ENARADA, New Delhi

By Ajay N Jha

When the entire globe started confronting economic challenges way back in 2006, Indian government boasted of 9 percent plus annual growth. When the loan crisis hit Europe, India pledged assistance of $ 10 billion.

The symptoms of fast decreasing economy had actually started since 2012 first quarter itself with fall in industrial production, fall of share market, fall in valuation of INR, fall in growth rate as well as the GDP. Yet the UPA II government was hopeful of sailing through the tide.

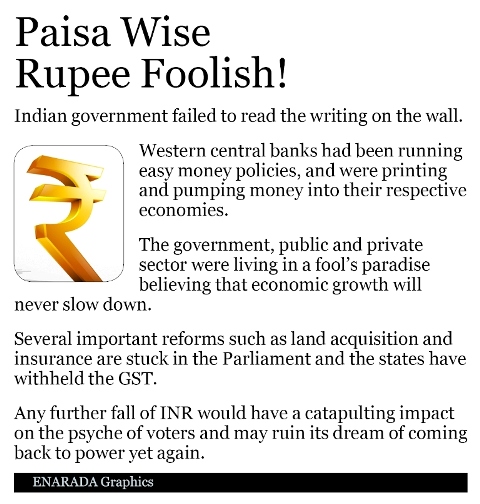

Not only the Indian government failed to read the writing on the wall, corporate India has also started landing in an equally messy situation on the debt that it has managed to accumulate over the last few years.

A report by Analysts Ashish Gupta, Kush Shah and Prashant Kumar of Credit Suisse estimated that the “gross debt of ten Indian corporate groups for the financial year 2012-2013 (i.e. the period between April 1, 2012 and March 31, 2013) stood at Rs 6,31,024.7 crore. Their debt has risen by 15 percent over the financial year 2011-2012 (i.e. the period between April 1, 2011 and March 31, 2012) interestingly, in the financial year 2006-07( i.e. the period between April 1, 2006 and March 31, 2007) the gross debt of these groups had stood at Rs 99,300 crore. So their debt has increased six fold in the period between March 31, 2007 and March 31, 2013.”

It was this situation which landed these top groups including Videocon, Adani, Essar, JSW, Reliance ADA, Vedanta, GMR, GVK etc., into serious trouble. The overall interest coverage ratio of these groups in 2012-13, stood at 1.4.

The interest coverage ratio is essentially a measure of the capability of a company to pay interest on its outstanding debt. It is calculated by dividing a company’s earnings before interest and taxes (EBIT or operating profit) for a year by the interest to be paid on the outstanding debt, for the same year. An interest coverage ratio of 1.4 essentially means that for every Rupee 1 of interest that the company has to pay, it makes Rs 1.4 of operating profit. This basically means that around 71.4 percent (1/1.4) of the operating profit of the ten groups cited in the report, will go towards interest payment. This is a very tricky situation to be in.

The interest coverage ratio of the ten corporate groups cited in the report has dropped from 1.6 as in FY 2011-12, to 1.4 in FY 2012-13 What this means is that in FY 2011-12, these groups would have had to pay 62.5 percent (1/1.6) of their operating profits to pay interest on their outstanding debt. That has now jumped to 71.4 percent. In fact, some of the groups have an interest coverage ratio of less than one which means that they are not making enough money to repay the interest on their debt. As the Credit Suisse analysts point out “Aggregate interest cover for these top ten groups has dropped from 1.6x to 1.4x. Interest cover ratios at groups such as Essar, GMR, GVK and Lanco are already under 1x Interest cover at Adani and Jaypee has also fallen to 1.5x.”

According to these analysts, the situation gets much worse if one takes into account the fact that the groups are currently not expending the entire interest cost in their profit and loss account. This is because the money raised through debt has been used to construct projects. A large part of these projects are currently under construction and haven’t come on stream. Hence, a lot of interest is currently being capitalised, which basically means that it is being shown on the asset side of a balance sheet and hasn’t been shown as an expense in the profit and loss account.

The depreciating rupee has been adding to the problem because a huge proportion of the outstanding debt of these corporate groups is in foreign currency. “Many corporates’ loans are 40-70 percent foreign currency denominated; therefore, the sharp depreciation in the rupee is adding to their debt burden. Adani Enterprise and Reliance Communications have the largest percentage of borrowings through forex loans,”say these analysts. The sliding INR means that these corporate groups will have to pay more rupees to buy dollars to repay their foreign currency loans.

All this debt also means that the situation can’t be good for Indian banks which have lent this money. As analysts Ashish Gupta and Prashant Kumar of Credit Suisse pointed out, “Over the past five years, Indian banks have witnessed strong (20 percent CAGR) loan growth. However, this growth is increasingly being driven by a select few corporate groups. In FY12, over 20 percent of the incremental loans came from just ten groups. The total debt level of these ten (Adani, Essar, GMR, GVK, JSW, JPA, Lanco, Reliance ADA, Vedanta and Videocon) has jumped 5 times in the past five years (40 percent CAGR) and now equates to 13 percent of the total bank loans and 98 percent of the net worth of the banking system.” The situation could have only gotten worse for Indian banks since then.

Moreover, interest rates in India over the last few years have been higher in comparison to interest rates abroad. This is primarily because the RBI had been raising interest rates to tackle high inflation. At the same time the Western central banks had been running easy money policies, and were printing and pumping money into their respective economies. With a surfeit of money going around interest rates abroad were thus lower, leading to the Indian corporates borrowing abroad rather than in India. Indian government helped corporates in this borrowing binge. Because of encouragement by policymakers at the Finance Ministry, RBI and Planning Commission. Among other things, corporates were permitted to access up to $500 million of ECB under the ‘automatic approval’ route every year, which got subsequently enhanced to $750 million.”

Now with the rupee rapidly against the dollar, all this debt will end up creating huge problems for these overleveraged corporate groups. One way out of this mess is by generating money through the sale of assets that these groups have. The trouble here is that who do they sell to?

A noted economic expert and commentator listed five reasons for present mess:-

1. The government, public and private sector were living in a fool’s paradise believing that economic growth will never slow down. The government allowed subsidies to burgeon, as rising oil prices were not passed on to consumers while public sector banks lent heavily to infrastructure projects of the private sector where revenues were more mythical. The private sector floated projects based on valuations of licenses and commodities rather than on future cash flows.

2. The illusion of high foreign exchange reserves made policymakers ignore a potential spike in Current Account Deficit (CAD). India’s foreign exchange reserves touched record highs of around $320 billion in February 2011 (around 11 months of import cover) but have plummeted by 12.5 percent since then to levels of $280 billion (around seven months of imports). CAD was financed by capital flows that led policymakers to believe that a high CAD would not impact the INR. Structural issues of oil and gold imports, rising inflation and high fiscal deficit was ignored until too late.

3. UPA II Government gave priority to growth over inflation. The focus on growth by all stakeholders concerned pushed inflation to the back seat. The RBI was castigated in public by both the government and the corporates for taking any action on inflation as it was felt that growth would suffer. The economy has suffered due to the wide fluctuations in inflation and policy rates, leading to the INR being dumped later on.

4. The government felt that India was too much of a growth story for the INR to fall. The noises made by the government when the INR touched Rs 57 in June 2012 suggested that the INR was being pulled down due to reasons other than macroeconomic factors. The RBI forced speculators to reduce long USD/INR positions while the government made noises on reforms and growth. The government and the RBI did not show urgency in tackling the INR fall last year and that has hurt them heavily this year.

5. Chidambaram has been touring the world to bring in foreign investments while the RBI has strangled liquidity and reintroduced Capital controls. Policymakers are not focusing on growth at the right time and markets know that policy actions cannot stem the fall in the INR, thereby making a case for wrong policies at the wrong time.

In addition, there are a few other areas where the Union Government has been sleeping over. At present several important reforms such as land acquisition and insurance are stuck in the Parliament and the states have withheld the GST. There are zero chances of reforms in the labor sector. Experts opine that the administrators should come up with new reforms that will bring back confidence in national economy. Reforms are urgently required in specific sectors like, Land acquisition, GST, Labor laws and FDI in retail. Red-tapism needs to be reduced and the SMEs have to be provided greater access to financial services. It is expected that these factors will help India climb the growth charts again.

Prime Minister Manmohan Singh has been trying his best to retrieve the situation with promises of governmental emphasis on infrastructural improvement through private-public partnerships. However, the government has gone back on several reforms such as liberalizing the retail fund, which has been expected for a long time now and all these have caused some major credibility issues for it. However, the general feeling among experts is that the government favors short term and populist decisions to deal with inflation instead of focusing for the long haul. A few analysts that the situation can be retrieved if the government takes some difficult steps like doing away with the fuel subsidy that is becoming less sustainable by the day and allow total foreign investment in the retail sector. It also needs to implement a direct tax code and eliminate tax evasion and corruption.

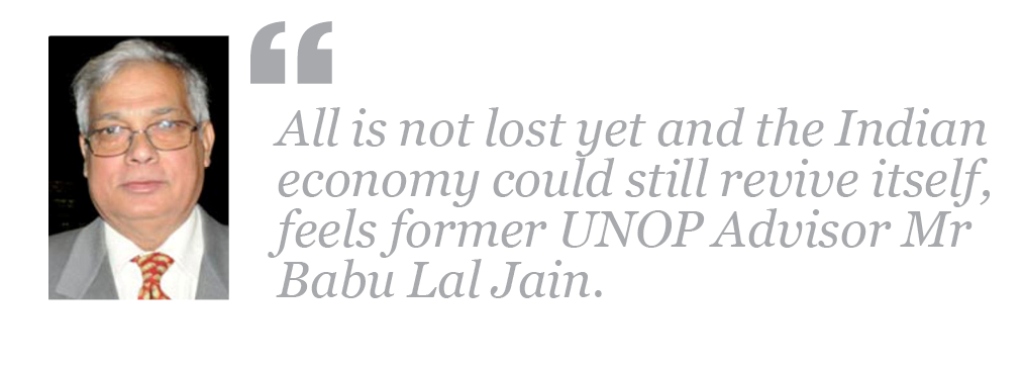

However, all is not lost yet and the Indian economy could still revive itself, feels former UNOP (United Nations Office on Partnerships) Advisor Mr Babu Lal Jain. He compared the present INR fall rate with the Eurozone debt crisis that reached its peak in mid2012. Greece was supposed to default, bond yields of Spain and Italy shot through the roof, the Euro was trading at multi year lows to the USD and equity markets across the world were at calendar year lows. Yet, the outcome was better, the Eurozone did not collapse and the Euro is trading 11 percent higher against the Dollar. “Just see that Greece is almost forgotten by markets, though the country itself is feeling the effects of austerity. India can still get over this crisis’ he affirms.

According to Mr Jain, the present rupee fall should be seen as a loud warning bell and politicians will not take the economy for granted and harp on pro citizen policies that actually hurt the citizens the most. Subsidies, freebies and tax exemptions lead to inflation, falling economic growth and a worthless currency. He says that the Brazilian Real is the only other currency that has depreciated more than the INR, falling by over 53 percent in the last two years and that happened because of cocky bureaucracy, corruption and weak infrastructure. On the other hand, India’s problems stem from overconfidence on growth, economic mismanagement, bureaucracy, corruption and weak infrastructure. “The INR fall is completely man-made and policymakers blaming the forthcoming withdrawal of the stimulus by the US Fed are pure nonsense” Says Mr Jain.

His prescription for reviving the Indian economy and stem the slide of INR include the following:-

1. Target the industry which can start manufacturing within a year.

2. Start aggressively targeting import substitution.

3. Get into the higher gear if IT, ITS and Cyber security. The world IT market is worth $ 2.17 trillion and Indian market does not exceed beyond $ 300 billion even today.

4. India has a great potential to upgrade capacity and get the best of expertise from within to address to it.

5. Indian corporates should come together to support the country in accelerating the infrastructure and import substitution and provide hands-on training to potential employees.

6. The Corporates must invest on their CSR not as a giveaway but as a part of their indirect business and roll back.

7. Make a two layer team of companies (top 100 and top 1000) and ask them to be onboard in preparing the recovering and recoup plan.

8. Seize the assets of those companies which cheated the country.

9. Make an appeal to Indians overseas to support India at this crucial juncture.

10. Bring Dollar interest at 8 percent for only persons of Indian origin.

On the face of it, these suggestions look quite attractive. However, their implementation would be quite a hard choice and that too, when the Congress led UPA government has been getting pilloried by opposition parties on various scams and scandals.

Added to its chagrin is the fast approaching LS polls. Under these circumstances, any further fall of INR would have a catapulting impact on the psyche of voters and may ruin its dream of coming back to power yet again. It remains to be seen how the Indian Prime Minister and Finance Ministrer wriggles out of this messy situation in the coming days.

(Posted on August 23, 2013 @ 8.30pm)

(Ajay N Jha is a veteran journalist from both Print and Electronic media. He is the President and CEO of WICS Global Communications. His email id is Ajay N Jha <ajayjha30@gmail.com> )

The views expressed on the website are those of the Columnists/ Authors/Journalists / Correspondents and do not necessarily reflect the views of ENARADA.

{kind=link}